Insight: Big debts loom over Thai tycoons’ bold bets

(Reuters) – Two Thai business tycoons, one a politically connected Chinese speaker, the other the son of a street vendor, have spent $27 billion on acquisitions in the past year, mainly abroad – more than all Thai firms spent overseas in the previous three years.

The billionaires – 74-year-old Dhanin Chearavanont and Charoen Sirivadhanabhakdi, five years his junior – personify Thailand’s bull market and Asia’s frothy credit, feeding on fast, cheap loans bolstered by a surging local currency.

The worry though is that they also represent the financial risks building inside Thailand and elsewhere in Asia amid signs of economic slowdown and tighter lending markets. Consumer growth needs to stay fairly robust to justify the valuations paid for these deals, said Standard Chartered analyst Nirgunan Tiruchelvam.

So far, Dhanin and Charoen look to be digesting their spoils without issue, but some warning bells are ringing about the high prices paid and the heavy debt load taken on – loans that are tied to real estate and a skittish Bangkok stock market that can swing sharply even when interest rates rise, let alone if there’s a credit crunch or steep economic slowdown.

“I’m a little concerned about Thailand, to be honest. It’s all debt. I’ve been in Asia long enough to remember how messed up Thailand was,” said a veteran Asia investment banker in Hong Kong, recalling the 1997 Asia financial crisis. “Financing was pretty cheap, interest rates were low. And once the music stopped ..?”

AUSPICIOUS

Early on April 23, bankers, lawyers and executives gathered in HSBC’s Hong Kong boardroom to sign the $6.6 billion purchase of Thai wholesaler Siam Makro by CP ALL, the retail arm of Dhanin’s CP Group conglomerate. According to some of those present, Dhanin’s son called for hush and counted down the seconds so his father could sign at exactly 8:45 Bangkok time – as advised by his feng shui consultant to maximize good fortune – revealing both Dhanin’s ability to command a roomful of powerful financiers and the Chinese influence on his personal and business life. The number 8 – linked by Chinese to prosperity – figures frequently in deals.

Dhanin’s father, Chia Ek Chor, left Guangdong in China in 1921 and, a quarter of a century later, renamed his seed shop Charoen Pokphand – Thai for “prosperity of consumers” – and began diversifying. Dhanin, the youngest son, a cockfighting fan at boarding school, has run the business since he was 30, growing it into a multinational with ventures across farming, retail and telecoms. His sons Suphachai and Soopaki help manage the vast empire, say people close to the family.

As of March, the Dhanin estate had an estimated net worth of $14.3 billion, according to Forbes. Gold and gem statues adorn CP’s Bangkok headquarters, and Dhanin’s neo-classical mansion, bristling with high-tech gear and arranged according to feng shui, is reckoned to be worth $30 million. The fluent Mandarin speaker has strong political connections in Beijing, and one of his businesses owns Shanghai’s largest shopping mall.

Dhanin paid more than 50 times Siam Makro’s price to earnings ratio after borrowing most of the money for the acquisition from banks – a hefty premium to any recent Asian retail sector deal. “What looks expensive today will be cheap in the long term. Siam Makro is a good asset,” Dhanin said then.

That’s a positive view shared for now by Standard Chartered’s Tiruchelvam given “a transformation in retail behavior that is in favor of these businesses.”

‘TAKEOVER KING’

Charoen, too, has taken advantage of frothy debt markets.

The Charoen-controlled entity that bought Singapore’s Fraser & Neave for $11 billion in January leveraged up the balance sheet of his flagship company Thai Beverage, quadrupling its debt to core earnings ratio – a key measure of its ability to pay back debt. Charoen has indicated a cash payout from F&N will pay down some of that business’s debt.

Ratings agencies remain wary. Standard & Poor’s, which has downgraded Thai Beverage’s credit rating, was critical about Charoen banking too much on the listed company to raise debt. “When a company shifts its risk tolerance so much in such a short period of time, it’s something you have to question at this stage,” Jean Xavier, a director at S&P, told Reuters.

Like Dhanin, Charoen has weathered crises before.

His father eked out a living by selling seafood omelets on the streets of Bangkok’s Chinatown. The sixth of 11 children, Charoen demonstrated a sharp business brain at a young age, graduating late from fourth grade as he devoted his study hours to selling toys to his classmates, according to a biography.

He quickly rose from a supplier to state-owned distillers to having his own producer’s liquor license, earning the “Whiskey Tycoon” moniker, though he himself is teetotal, say bankers and businessmen who have worked with him. Backed by his father-in-law, Charoen bet on the financial sector, buying stakes in First Bangkok City Bank and Maha Thankit Finance and Securities – both of which collapsed during the 1997 Asia financial crisis.

Dubbed the “Takeover King” for his incisive acquisitions of stakes in companies struggling after the crisis – he expanded closer to home than Dhanin, focusing on Southeast Asia – Charoen is now grooming his children, including eldest son Thapana, to manage his TCC empire, which boasts a string of luxury hotels spanning four continents. His wife Wanna has been described as his “No. 1-1/2”, rather than Number 2, in recognition of her major role in managing the family business – estimated by Forbes to be worth $11.7 billion.

“The Sirivadhanabhakdi family are very humble, low-key people,” said Prinn Panitchpakdi, Thai country head at broker CLSA. “They’re very religious and attend Buddhist ceremonies.”

LIQUIDITY GLUT

Dhanin and Charoen are being showered with money for deals by banks which, says Standard & Poor’s Xavier, are extending loans as Asia has a liquidity glut – partly a spillover from Western central banks pumping funds into their markets.

“Valuations are secondary. It’s how much money is available,” said another banking source who has covered Thailand for many years. “Every bank is willing to bridge the entire acquisition off their own balance sheet.”

Siam Commercial Bank, the lead adviser to CP ALL on the Makro deal, offered so much money to the buyer that it needed a special Bank of Thailand waiver, according to a person familiar with the matter. And HSBC was comfortable enough to sit on both sides of that deal, advising the seller, Dutch trading firm SHV Holdings, and funding the buyer, CP ALL.

According to the person, banks were given very short notice that a deal was imminent, but still managed to pull together the $6 billion loan within a week – an extraordinarily short period of time for such a large amount.

For Dhanin’s $9.4 billion purchase of HSBC’s stake in China’s Ping An Insurance late last year, [ID:nL4N09F1OO] UBS offered a short-term facility worth $5.5 billion. [ID:nL3N0CJ0JY] Dhanin has said the Ping An loan was no more than $2.6 billion. To help finance the Fraser & Neave buy, Charoen’s Thai Beverage borrowed S$3.3 billion from seven banks for five years, replacing an earlier bridge loan, while his TCC family vehicle took a further S$9 billion jumbo bridge loan – the biggest by a Thai borrower – Thomson Reuters publication Basis Point reported.

Bridge loans are typically short-term and widely used by companies in M&A deals, replaced later by larger or longer-term financing.

“From a ratings point of view, in the case of ThaiBev/TCC, the track record of integrating very large acquisitions is largely untested,” said S&P’s Xavier. “When you have operated at low leverage for a long time and your debt load spikes very suddenly, how will the company manage a downturn?”

Neither Dhanin nor Charoen was available for interview for this article.

The Thai stock market is up nearly 9 percent this year, but has dropped more than 8 percent in the past three weeks. Thailand’s central bank cut interest rates to 2.5 percent last month after weak first-quarter GDP data.

“If you stumble a little, if that begins to unravel, whoever lent them money is going to have some serious concerns. It’s all margin loans … very tied to the market,” said an M&A adviser based in Singapore.

From: http://www.reuters.com/article/2013/06/09/us-thai-tycoons-insight-idUSBRE9580G520130609

Review

English news of Thailand

-

Google Street View driver made to swear on statue of ...

13,288 views

No Comments

Twins Special, Maker of Best Thai Boxing Gloves, Muay...

11,636 views

No Comments

SE Asia stocks mostly up, Thai stocks flat

11,981 views

No Comments

Burmese Refugees Remain in Limbo by Thai Border Despi...

12,010 views

No Comments

Six killed by Thai soldiers during 2010 crackdown on ...

11,305 views

No Comments

Thai Government, Opposition at Odds Over Amnesty Bill

8,140 views

No Comments

Thai anti-government group stages protests

7,887 views

No Comments

Thai Amnesty Push Risks Protests as Stocks Slide

8,285 views

No Comments

Thai Bitcoin exchange suspends trading

8,064 views

No Comments

Oil Spill Spreads Along Thai Island, Threatens Mainland

7,935 views

No Comments

Thai central bank rules Bitcoin to be illegal

8,232 views

No Comments

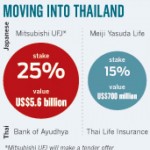

Meiji Yasuda buys 15percent stake in Thai Life Insurance

7,964 views

No Comments

Lion Fights: Tiffany Van Soest discusses sponsorship ...

14,149 views

No Comments

Megastore for Thai Monks Brings One-Stop Retail to Bu...

9,862 views

No Comments

19 dead in Thai bus crash

8,411 views

No Comments

Foreign Tourists Among Injured in Thai Train Derailment

8,424 views

No Comments

Tourists among 23 hurt in Thai train derailment

7,739 views

No Comments

Muy Thai, the peaceful mixed martial art

8,361 views

No Comments

Thai university apologizes for Hitler banner

7,629 views

No Comments

Thai monks disrobed for drug use

8,411 views

No Comments

Thai Palm Oil Exports Seen Rising by Oil World as Out...

7,870 views

No Comments

American hacked to death over $1.60 cab fare, Thai po...

8,244 views

No Comments

Local restaurant owner capitalizes on model, aims to ...

8,300 views

No Comments

Thai government reverses rice price cut

8,168 views

No Comments

Thai Economy May Be Vulnerable To Another Shock Due T...

7,909 views

No Comments

Thai peace talks brokered by M’sia hit a dead end

9,588 views

No Comments

Thai-Cambodia Border Decision Risks Renewing National...

7,268 views

No Comments

Thai Basil promises good flavor, service

8,382 views

No Comments

Thai AirAsia undaunted despite rise in competitors

8,403 views

No Comments

Thai Company Reinstates Burmese Workers after Protest

8,018 views

No Comments

Thai travellers told to avoid smog-hit Singapore

7,824 views

No Comments

Thai threat to pre-season plans

8,770 views

No Comments

Buddhist monks arrested over Thai child sex abuse claims

8,664 views

No Comments

Tablets thrust Thai classrooms into digital era

7,962 views

No Comments

Fueled by cheap credit, two Thai tycoons spend $27 bi...

7,982 views

No Comments

Insight: Big debts loom over Thai tycoons’ bold...

8,382 views

No Comments

S.E.C. Freezes Assets of Thai Trader in Smithfield In...

8,810 views

No Comments

Thai Spring to target Thaksin online

7,836 views

No Comments

Lyman Good ready for next Bellator fight after victor...

8,791 views

No Comments

Thais told to drink milk to boost height

8,715 views

No Comments

Thai Protesters Latest to Don ‘Guy Fawkes’...

8,442 views

No Comments

Thai Fishing Industry Is Using Slave Labor To Catch T...

8,366 views

No Comments

Chalerm gets PM’s nod to lead Thai delegation i...

8,375 views

No Comments

Troops Killed Italian Reporter

8,266 views

No Comments

In Thailand’s Schools, Vestiges of Military Rule

8,399 views

No Comments

Bomb explodes at market in Thai capital, injures seven

8,656 views

No Comments

Deadly blast targets Thai soldiers

9,413 views

No Comments

Abe welcomes Thai leader, urges eased rules on food i...

9,043 views

No Comments

Thai-inspired lemongrass mojitos with basil

9,066 views

No Comments

Care needed with Thai biodiversity

9,276 views

No Comments

Anyone for Thai Green Curry crickets? Or BBQ worm cri...

9,647 views

No Comments

Thai Spring launches online campaign against Yingluck

8,650 views

No Comments

Thai ghost film remake appeals with funny twist

8,931 views

No Comments

QA signs codeshare pact with Thai carrier

8,984 views

No Comments

Small attack on Thai newspaper has large implications

8,768 views

No Comments

Thai ad firm back in Indochina

11,639 views

No Comments

Court disqualifies Pheu Thai MP

9,625 views

No Comments

The Strange Thai Insurgents Who Like Sorcery and Get ...

8,509 views

No Comments

Thai hurt in Philippine volcano blast

8,695 views

No CommentsNSC sees poll win boosting peace talks

8,473 views

No Comments

Kerr takes over after Thai teen stumbles

8,750 views

No Comments

Thai 17-year-old Jutanugarn leads LPGA in Virginia

14,903 views

No Comments

Watch This Crafty & Awesome Thai Sweded Trailer ...

9,091 views

No Comments

Thai King Recovering From Mild Lung Inflammation

8,602 views

No Comments

Lee, Thai teen win India Open titles

15,267 views

No Comments

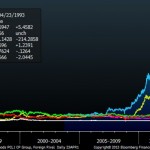

Thai Billionaire’s 7-Eleven Reaps 1,700% Gain: Chart ...

8,354 views

No Comments

Noble borrows ADB’s rating to borrow Thai baht

8,732 views

No Comments

CP All Offers $6.6 Billion for Thai Retailer Siam Makro

8,712 views

No Comments

What should Thai Prime Minister Yingluck Shinawatra’s...

8,176 views

No Comments

Happy Thai team home from The Hague

8,445 views

No Comments

Naples Family Fitness Center Introduces Thai Bodywork

8,366 views

No Comments

Thai residents in shock after Boston blasts

7,927 views

No Comments

Thai horror film-makers sink teeth into south-east As...

9,439 views

No Comments

3 Thai universities named among 100 best in Asia

8,814 views

No Comments

A bright year for Thai cinema

8,759 views

No Comments

Jet Tila Appointed Thai Cuisine Ambassador

8,455 views

No Comments

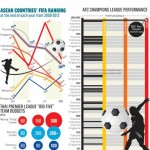

The rise and fall of Thai soccer

8,982 views

No Comments

Thai New Year Festival, LA Phil & More

9,823 views

No Comments

Chinese, Thai PMs pledge to advance ties, China-ASEAN...

8,915 views

No Comments

Do Asean countries offer benefits of diversification ...

8,766 views

No Comments

Chiang Mai does Thai on Wichita’s south side

8,519 views

No Comments

Netizens roused by sexy calendar, music video

139,611 views

1 Comment

Durian import moratorium does not smell sweet to Thai...

17,463 views

No Comments

Thai soldiers killed in roadside bombings

9,948 views

No CommentsThai women warned over sex trade gangs

9,498 views

No Comments

Thai AirAsia goes for bigger market share

8,393 views

No Comments

Green procurement ideas inspire Thai businesses

9,212 views

No CommentsWorld’s craziest free kick? Thai side Muangthon...

8,845 views

No Comments

Thai kids not interested in growing up to become prim...

8,621 views

No CommentsThai officials seize smuggled rhino horns hidden in l...

10,416 views

1 Comment

“The foreigner got in the way”: Thai gang...

8,424 views

No Comments

Thai Govt Urged to Reveal Whereabouts of 73 Rohingya ...

8,737 views

No Comments

Chi Tan Thai’s 1978 journey to Toronto as one o...

10,616 views

No Comments

Thai community in shock as monks die in car smash

13,896 views

2 Comments

Freed son tells of Thai nightmare

9,616 views

No Comments

Modern life takes toll on Thai monks

9,585 views

No Comments

My Muay Thai Training: Implementing a strategy

9,182 views

No Comments

2 for $25: Orchids Thai

9,392 views

No Comments

Thai hopeful Rida in spotlight at Miss Universe

10,067 views

No Comments

Thai, Burmese govts back Dawei project

9,160 views

No Comments

Thai carmaker’s office bash turns to brawl; 30 ...

8,329 views

No Comments

Sway Thai Now Open On South 1st

8,817 views

No Comments

Thai PM visits violence-torn south after deadly attacks

8,903 views

No CommentsThai students drop in world maths and science study

8,252 views

No Comments

Schaefer urges Thai protest

8,765 views

No Comments

Coffee from Thai elephant’s dung costs $50 per cup

10,141 views

No Comments

Muay Thai fighters battle for championship titles in ...

9,135 views

No Comments

Thai king calls for unity in rare speech

8,802 views

No CommentsUPDATE 1-Thai court rejects complaint against 3G auction

9,055 views

No Comments

Thai pop star Natthew expresses interest in collabora...

9,288 views

No Comments

Tailgating Recipe: Mike’s Thai Style Baby Back Ribs

51,781 views

No CommentsThai PTTEP offers near 13 percent discount for $3.1 b...

8,473 views

No Comments

Thai ‘red shirt’ protest leaders to go on trial

8,629 views

No Comments

Thai Prime Minister faces no-confidence vote

16,778 views

No CommentsThai banks ‘must think regionally’

8,658 views

No Comments

Kingsgate Eyes 2013 Launch of Delayed Thai IPO

8,844 views

No Comments

Why Thai women cut off their husbands’ penises

9,139 views

No CommentsMost Viewed

139,611 views112,367 views100,237 views97,907 views79,460 views68,941 views